Bookkeeping, collecting receipts, and managing your rent payments isn’t always the most exciting part of property management. But to run a successful business, you’ll need a well-oiled accounting system.

To get that system in place, we’ve created this guide (and video) to walk you through every step of the property management accounting process.

What you’ll learn in this guide:

- How to set up your accounting systems properly

- How to set up your bank accounts

- Tips and shortcuts to save you time and money

- Worry-free solutions that automate your bookkeeping

Let’s dive in!

Property Management Accounting: Article Guide

What Is Property Management Accounting?

Property management accounting is the systematic tracking and recording of all financial transactions for rental properties and property management businesses. This includes rent collection, property expenses, maintenance costs, insurance payments, and tax obligations.

Is Property Accounting Difficult?

While there are nuances to property accounting, it’s no more difficult than any other accounting. There are, however, certain accounting actions that make property management accounting unique.

Staying on top of bookkeeping is incredibly important. It allows you to make better decisions about how you’re running your business and how you’re managing your clients’ properties. Getting property management accounting right saves you time throughout the year. It also prepares you for tax season and major financial events like quarterly meetings with owners or your HOA.

Bad fundamentals, on the other hand, can lead to missing tenant payments, miscalculating your cash flow, and even compliance issues that could lead to fines—for example, penalties for not filing 1099 forms can range from $60 to $680 per form. These problems will ultimately stifle your business growth.

What Does a Property Account Manager Do?

To make things easier, you can work with an accountant to handle the financial aspects of your business. They are in charge of accounting, asset management, and bookkeeping duties, to ensure you’re tax compliant and your books are accurate.

Property Management Accounting Terms You Should Absolutely Know

Before we dive into more of the nuts and bolts of accounting, let’s go over some key property management accounting terms. These are terms you might have already heard:

Core Financial Terms

- Accrual Accounting: Recording revenues and expenses when earned or incurred, regardless of cash movement—providing a more accurate picture of financial health by matching income and expenses to their actual period.

- Cash Accounting: Recording revenues and expenses only when cash is received or paid—offering a straightforward view of cash flow that’s particularly useful for smaller operations.

- Credit: An entry that decreases assets or increases liabilities and equity, representing amounts owed to vendors, lenders, or other parties.

- Debit: An entry that increases assets or decreases liabilities and equity, representing amounts paid or owed for operational expenses.

- Generally Accepted Accounting Principles (GAAP): Standardized guidelines ensuring consistency, transparency, and accuracy in financial reporting—covering revenue recognition, expense matching, and disclosure requirements.

- General Ledger (G/L): A comprehensive record of all financial transactions, organized by assets, liabilities, equity, revenues, and expenses.

- Accounting Period: A specific timeframe (monthly, quarterly, or annually) for recording and reporting financial transactions to track performance consistently.

- Bank Reconciliation: Matching accounting records with bank statements to identify and resolve discrepancies, ensuring cash record accuracy.

- Bookkeeping: Recording all financial transactions related to property operations, including rent income, maintenance expenses, utilities, and other activities.

Property-Specific Terms

- Asset: Resources with dollar value owned by the company or clients—including physical properties (buildings, land) and financial assets (cash, accounts receivable, investments).

- Depreciation: Allocating the cost of tangible assets over their useful life to reflect gradual wear and tear on buildings, equipment, and other property assets.

- Fixed Cost: Expenses that remain constant regardless of occupancy levels—including property taxes, insurance, and permanent staff salaries.

- Overhead: Ongoing administrative and operational expenses not tied to specific properties—such as management salaries, office supplies, utilities, and general business costs.

- Chargeback or Expense Recovery: Recouping costs initially paid by the property management company by billing tenants or clients for utilities, maintenance, or other services.

- Revenue: All income generated by properties or the business—including rent payments, service fees, parking fees, laundry services, and other income sources.

Accounting Process Terms

- Accounts Payable: Amounts owed to vendors or suppliers for goods and services received but not yet paid—including maintenance bills, utilities, and operational expenses.

- Accounts Receivable: Money owed by tenants or clients for rent, services, or charges—requiring tracking and management to ensure timely collection and accurate reporting.

- Allocation: Distributing funds to different general ledger accounts, periods, or properties to ensure each area has necessary funds for expenses and efficient operations.

- Equity: The residual interest in company assets after deducting liabilities—representing ownership value including initial investments, retained earnings, and capital contributions.

- Expense: Costs incurred in operating and maintaining properties—including maintenance, repairs, utilities, property taxes, insurance, and administrative expenses.

- Liability: What the business or property owner owes to another party—including loans, mortgages, accounts payable, and accrued expenses.

Property Management Accounting Basics

Building strong accounting systems saves hours on routine tasks. With the right property management bookkeeping basics, you can manage accounts consistently and accurately.

Here are the five best ways to build your foundation:

1. Open a Separate Basic Account

The first and arguably most important step is to ensure that you have a proper bank account structure for your business so that funds aren’t passing through a single bank account (which may be illegal in most states). This structure varies depending on the size and scope of your business, but here are the four main bank accounts you’ll generally need to open:

- Property management trust account

- Security deposit account

- Operating account

- Property management reserve (optional)

Several states require security deposits to be held in separate escrow accounts, so funds are able to be accessed when residents move out. If your state allows it, consider placing your security deposits in a trust.

2. Establish a Property Management Chart of Accounts

A chart of accounts for property management is a way to organize all transactions for every property you manage. When set up right, it effectively categorizes each transaction within the general ledger, making property management accounting much easier.

Depending on the complexity of your business, you can start with an Excel spreadsheet or use a comprehensive solution such as Buildium to build it automatically for you.

The chart of accounts is made up of five major types of accounts:

- Assets

- Liabilities

- Equity

- Income

- Expenses

How to organize your chart of accounts

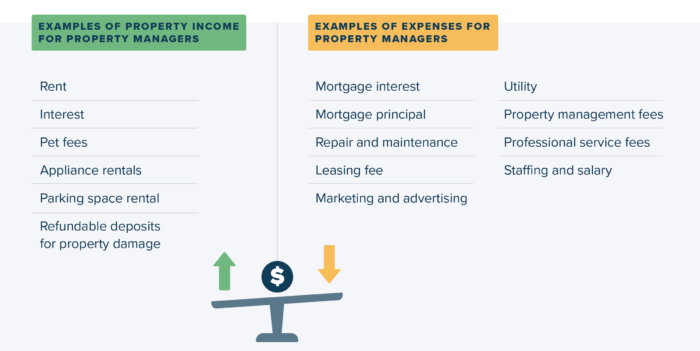

As mentioned above, the five types of transactions listed in a chart of accounts include assets, liabilities, equity, income, and expenses. You can then list categories for each type. For example, under income you can list rent, pet fees, appliance rentals, or parking fees.

Assets

Ensure you’re differentiating current assets with fixed assets. Current assets are variable and include escrow, reserve accounts for insurance, your bank accounts, taxes, capital expenditures, and interest.

Fixed assets are funds tied to your properties and business, including the monetary value of each property and the improvements made on them.

Expenses

Just like your assets, you can categorize each expense by taxes, software, supplies, utilities, repairs, bank fees, cleaning costs, travel expenses, etc.

Liabilities

Liabilities can be categorized between current and long term. Accounts payable, rent due, prepayments, security deposit liability, owner-held security deposits, and note payable.

Want more detail? We’ve put together a guide on setting up an air-tight chart of accounts that will walk you through everything you need to know, with expert advice and even an itemized list of what to include.

3. Decide Between Cash and Accrual Accounting

WIth cash accounting property managers record money as it is received and paid from their bank accounts. Accrual accounting records revenue and expenses when they occur, rather than when the money moves.

4. Decide Between Single-Entry or Double-Entry Bookkeeping

When keeping records, you start by recording detail in a general journal, the initial record where all financial transactions are initially recorded in chronological order. This journal includes detailed information about each transaction, such as the date, accounts affected, amounts, and a brief description. The general journal serves as the first point of entry for financial data before it is posted to the general ledger.

The general ledger consolidates all the transactions recorded in the general journal. It organizes these transactions by account, allowing your team to see the cumulative effect of all transactions on each account.

Single-entry bookkeeping is simply when all financial items are recorded one time in a general ledger. Some smaller property management companies opt for this method of bookkeeping for its simplicity, even though it is more prone to errors and has several limitations

Double-entry bookkeeping is more common and usually recommended for property management. Most property management companies need to track more than just cash flow.

With double-entry, every transaction is recorded twice: once as debit and once as credit. This helps you distinguish between different income sources (rent vs late fees) and track where money was deposited.

5. Manage Invoices and Receipts

Whether through accounting software or a more comprehensive property management solution like Buildium, keep a habit of maintaining a record of all statements for money going in and out of your business; it’s a best practice to store forms, W-9s, and payment records for at least four years. Set up a regular reporting schedule and be sure the numbers are checked thoroughly on a regular basis.

Property Management Trust Accounting Procedures

As a property manager, you’re handling other people’s money on a daily basis. Trust accounts are a valuable way to help you keep your owners’ assets organized, stay compliant, and reconcile accounts through more accurate reports.

Trust accounting basically means when a third party—in this case, a property manager—holds funds for the benefit of (in trust for) a beneficiary, the property owner. Having a trust account helps to keep your operating capital separate from the rent and payments you collect from residents.

Dos and Don’ts of Trust Accounting

Do make sure that you have a trust account in place for all payments you receive from residents, not just security deposits. When setting up a trust, the signee should always be the property management business owner or a bonded employee. The same amount of care to keeping your trust accounts up to date. Every 6 months to a year, make sure that the property owner (beneficiary) information for your trusts is accurate.

Do not grant non-bonded employees the ability to release funds from your trust accounts. That includes restricting ACH, billpay, and wire access. Also avoid using signature stamps to sign a trust agreement or other forms of banking authorization. Because these stamps are legal, authorized signatures, you won’t be able to claim fraud if an employee or others use your stamp for unauthorized activity.

Trust accounts are a necessary and useful tool to keep your funds organized and compliant with regulations, especially as you take on more owners, but they come with their own set of rules and risks. Learn more about how to set trust accounts up correctly.

Property Accounting Reports You Should Know

Reports are versatile tools that provide high-level overviews for investors or detailed breakdowns for monthly meetings. Here are the four reports that will make the biggest impact on your business.

Deep Dive: Knowing your books: which property accounting reports matter most?

Owner report or rental owner statement

| Report Type | Purpose | Key Information |

|---|---|---|

| Owner Statement | Shows property investment performance | Income/expenses by type, net income/loss, security deposits, capital contributions |

| Income Statement (P&L) | Documents cash flow for partners/shareholders | Management fees, expenditures, taxes, salaries, insurance premiums |

| Rent Roll | Predicts expected revenue | Lease dates, recurring charges, market rental values, vacancy status |

| Budget vs Actual | Compares projections to reality | Variances for budget adjustments and cash flow planning |

This report paints a picture of how the property owner’s investment performs at the beginning and end of every period. This accounts for all the money entrusted to you in an easy-to-understand matter. Here’s what comes with an owner report:

- Property address

- Contact information

- Beginning, end and statement dates

- Beginning and end balances

- Income, broken down by type

- Expenses, broken down by type

- Net income or loss

- Security deposits

- Early payments

- Capital contributions by owner

- Required reserve and operating levels

- Funds received but not yet deposited

Detailed Income Statement or Profit & Loss (P&L) Statement

An income statement documents your cash flow during a month, quarter, or year, so that your partners and shareholders are given accurate records of your company financials. These include:

- Beginning and end dates

- Income

- Property management fees

- Contributed capital

- Tax credits

- Profit from sale of assets

- Adjustments to previous assumptions

- Investment income

- Interest received

- Expenditures

- Taxes

- Rent

- Equipment

- Interest

- Salaries and wages

- Consulting fees

- Advertising and marketing costs

- Legal fees

- Accounting fees

- Software fees

- Insurance premiums

- Depreciation and amortization

Rent Roll

The rent roll report predicts expected revenue based on historical data. Owners use this report to see how they’re pacing against their financial goals. You’ll also see which units are vacant, which leases are up for renewal soon, and which tenants are on month-to-month leases.

The report includes:

- Lease dates

- Recurring charges

- Estimated market rental value

- Sum of all deposit amounts

Depending on how hands-on they are, owners might request the details captured in these reports often, and with little notice. Luckily, Buildium allows you to generate and download rent roll reports with just a few clicks.

Budget vs Actual Report

This report identifies the disparity between your projections and reality, which allows property managers to adjust their budgets and plan for potentially unexpected costs or cash flow issues.

Reports in Just a Few Clicks

No matter the type of report, you’ll want easy access to your accounting data and a way to share that data with owners. Buildium lets you generate and save accounting reports easily, and then send those reports to clients or other members of your team—all within the same platform.

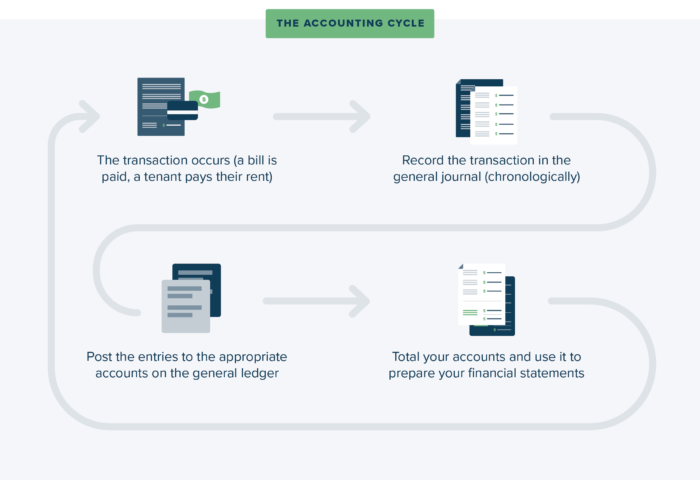

The Property Management Accounting Cycle

Having learned about all the different aspects of property management accounting, let’s see how it all fits together. There are four major steps that take place:

- The transaction occurs (a bill is paid, a tenant pays their rent)

- Record the transaction in the general journal (chronologically)

- Post the entries to the appropriate accounts on the general ledger

- Total your accounts and use it to prepare your financial statements

Actionable Tips: Property Management Accounting Best Practices

Now that we’ve talked through the basics of property management accounting, let’s go through ready-to-use tips that turn property accounting into an asset for your business.

Reconcile Accounts Monthly

Reconciling is the process of ensuring that your records match the money you’ve actually spent. Maintaining a habit of reconciling your accounts at the end of every month helps you find typos, duplicates, missing entries, and bank errors early.

Stay Cash-Flow Positive

Cash flow is how much money you have left over at the end of a measured period of time after collecting rent and paying out your expenses. Making the wrong investments, either in a property or in your business, can be a money sink for you and your clients, creating a negative cash flow. The higher the cash flow in the accounts you manage, the more money you’ll have on hand to make upgrades, grow your business, and pay off any debt. As obvious as this is, it’s one of the best ways to stay in the black is to proactively stay on top of accounting!

Have a Rainy Day Fund

It’s important to have a safety fund so you’re not struggling with unforeseen expenses. Work out the size of a reserve fund with rental owners, so you can stay ahead of the unexpected.

Be sure it’s liquid, or you’re able to tap into it with no risk of penalties or fees. Advisors typically recommend three to six months of expenses in your rainy day fund.

Essential Property Management Accounting Software Features

In the vast ecosystem of property management software, how do you choose the best accounting system for you?

We’ve developed several in-depth posts to help you answer that very question. We recommend reading this article on the benefits of purpose-built accounting software along with this guide on six features to look for in software, before diving into these head-to-head comparisons of specific property management accounting platforms:

- Should You Use Quickbooks for Property Management Software?

- 10 of the Best Rental Property Accounting Software for Better Bookkeeping in 2026

- 5 of the Best HOA Accounting Software Solutions in 2026

Choosing the right one will help you run and scale a growing portfolio, but they’re not all created equally. A purpose-built property management accounting solution should have the following features:

Automatic Bank Reconciliation

Reconciling your accounting records with your banks can be excruciatingly time consuming. One of the biggest timesavers is a software that automatically reconciles each check, deposit, and expense to minimize clerical errors that may end up being extremely costly. Automate reconciliation so you can generate accurate balance sheets, income statements, and rent rolls in real time.

Chart of Accounts

A chart of accounts categorizes all your financial transactions—which can be created automatically in an effective property management software. Instead of worrying about integrating your accounting software with your spreadsheets and your property management software, find a software that does it all in one place—and securely.

Advanced Security

A non-negotiable feature you should look for is the ability to lock your books when you’re ready to file, so it can’t be accidentally or purposefully tampered with—so your reports remain accurate.

Online Rent Payments

Digitizing your online rent payments allows you to record every rent payment you receive automatically. And it makes paying rent much easier for your tenants as well. Automating this will save you a ton of time and most accurately track your transactions. A top payment portal also provides a record of previous payments and allows you to accept rental applications and other fees directly online.

1099 eFiling

If you’re like most property managers, tax season may cause big headaches. An effective property management software will allow you to minimize the hassle by automatically e-filing your 1099 with the IRS, which is especially important since the agency requires electronic filing for businesses that file 10 or more information returns.

Accounts Payable

Any property management accounting software you choose should have automated accounts payable. Buildium, for example, includes calculators that show you what you owe your owners, your vendors, and yourself.

It also converts work orders into bills, includes online payments, and allows you to set up recurring payments, as well.

Of course, every business is different, and it’s always a good idea to talk with a professional CPA to understand requirements and details you should look out for that are specific to your company, your clients, and where you operate.

Building a Strong Financial Foundation for Your Property Management Business

Getting your property management accounting right is about more than just balancing the books. It’s about building a financial foundation that supports clear decision-making, keeps your owners informed, and positions your business for growth. By setting up the right bank accounts, understanding key accounting principles, and following compliance procedures, you create a system that works for you, not against you.

A purpose-built platform brings all these pieces together, helping you manage everything from rent collection to financial reporting in one place. This gives you the accuracy and organization needed to run your operations efficiently and confidently.

To see how a dedicated platform can put these principles into practice for your business, you can test Buildium out with a 14-day free trial or guided demo.

Frequently Asked Questions

What Is Property Management Accounting?

Property management accounting is the specialized practice of tracking financial transactions for rental properties and property management businesses to maintain accurate records and regulatory compliance.

How Do You Set Up Your Property Management Accounting?

Start by establishing a chart of accounts, choosing property management software, and implementing regular bank reconciliation procedures. Train your staff on GAAP principles to maintain consistency and accuracy.

What Does a Property Account Manager Do?

A property account manager provides support for utility billing programs, monitors property satisfaction, and helps with account management tasks.

What is Property Management GAAP Accounting?

GAAP accounting follows standardized guidelines for financial reporting to ensure consistency, transparency, and regulatory compliance. Learn more about GAAP here.

What Is the Best Accounting Software for Property Management?

Buildium is a popular choice offering rent collection, maintenance tracking, and financial reporting for all property types. Try it with a 14-day free trial.